Inflation as Good News: US Sentencing Commission Raises Bar on Loss Thresholds

Individuals facing federal fraud and tax evasion charges may soon see lower advisory guideline ranges under proposed Sentencing Guidelines amendments.

On April 16, the US Sentencing Commission unanimously voted to adopt amendments that, among other changes, adjust the monetary tables used to calculate sentences for fraud, tax evasion, and other economic crimes to account for inflation. This is the first inflation-based update to these tables in more than a decade.

How Sentencing Guidelines Amendments Are Enacted

The federal Sentencing Guidelines are advisory and serve as a starting point for federal judges. The US Sentencing Commission — an independent, bipartisan agency — updates the Guidelines through an annual amendment cycle: it proposes changes, solicits public comment, and votes on whether to adopt them. The amendments adopted on April 16 will be submitted to Congress on May 1, and, absent congressional action, will take effect on November 1.

Sentencing Commission Increases Loss Amounts

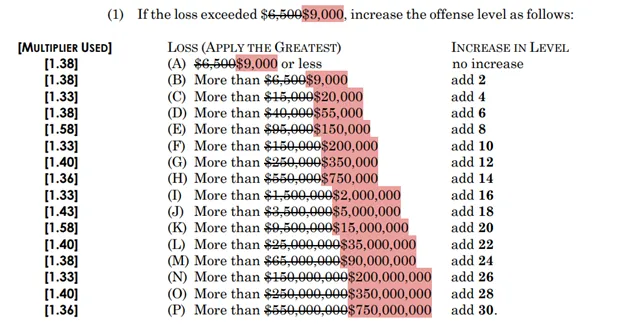

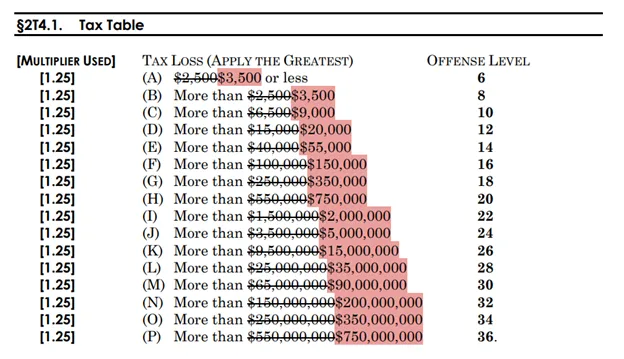

One of the most consequential changes for individuals under investigation for or charged with financial crime cases is an inflationary adjustment to the Guidelines’ monetary tables. In fraud and tax cases, the loss amount is often the primary driver of the recommended range. The Guidelines increase the offense level based on where the loss falls within specified dollar thresholds; higher offense levels generally mean longer recommended prison terms. The amendment increases those thresholds across the board to reflect inflation.

Under the current fraud loss table in §2B1.1, losses over $550,000 trigger a 14-level increase and losses over $9,500,000 trigger a 20-level increase. Under the amended table, those thresholds rise to $750,000 and $15,000,000. As a result, a $600,000 loss increases the offense level by 14 levels under the current table but will result in a 12-level increase under the proposed loss table. Under the current tables, a $12,000,000 loss results in a 20-offense level increase, but under the amended level that same loss would result in an 18-offense level increase.

The tax table in §2T4.1 has also been adjusted. Under the current table, losses over $1,500,000 result in a 22-offense level increase; yet under the amended table, losses over $2,000,000 result in the same 22-offense level increase. For example, a $1,600,000 tax loss currently leads to an offense level increase of 22; but under the proposed table this tax loss would lead to a level 20 under the amended table.

The revised loss tables appear at the end of this alert.

Sentencing Advocacy Before and After November 1

These amendments are a meaningful development for individuals charged with, or under investigation for, federal financial crimes. Because the thresholds are higher, many defendants will face lower recommended guideline ranges than under the current Guidelines.

Practically, a two-level reduction can mean months — and sometimes years — less time in custody, depending on criminal history and other factors.

As a general matter, courts apply the Guidelines in effect at sentencing. Accordingly, sentencings after November 1 will apply the new, more favorable loss tables. For sentencings scheduled before that date, defense counsel may seek an adjournment to a date after the amendments take effect. Counsel may also ask the court to consider the forthcoming amendments when requesting a variance.

ArentFox Schiff attorneys regularly represent clients in fraud and tax investigations and prosecutions and can use these amendments to pursue more favorable sentencing outcomes.

Excerpts From US Sentencing Commission’s Proposed Amendments

The following tables, created by the US Sentencing Commission, show how the adopted amendments change the loss tables. Values highlighted in red are expected to be effective on November 1.

Changes to Loss Table for §2B1.1 (Applicable to financial crimes such as larceny, embezzlement, fraud, and counterfeit). See US Sent’g Comm’n, Amendments to Sentencing Guidelines (Preliminary) 2 (April 2026) (link).

Changes to Loss Table for §2T4.1 (Applicable to tax crimes, including evasion and fraud).

See US Sent’g Comm’n, Amendments to Sentencing Guidelines (Preliminary) 10 (April 2026) (link).

Contacts

- Related Practices