DOJ Announces Corporate Enforcement and Voluntary Self-Disclosure Policy for All Criminal Cases

On March 10, the US Department of Justice (DOJ) announced its first uniform Corporate Enforcement and Voluntary Self-Disclosure Policy (DOJ CEP).

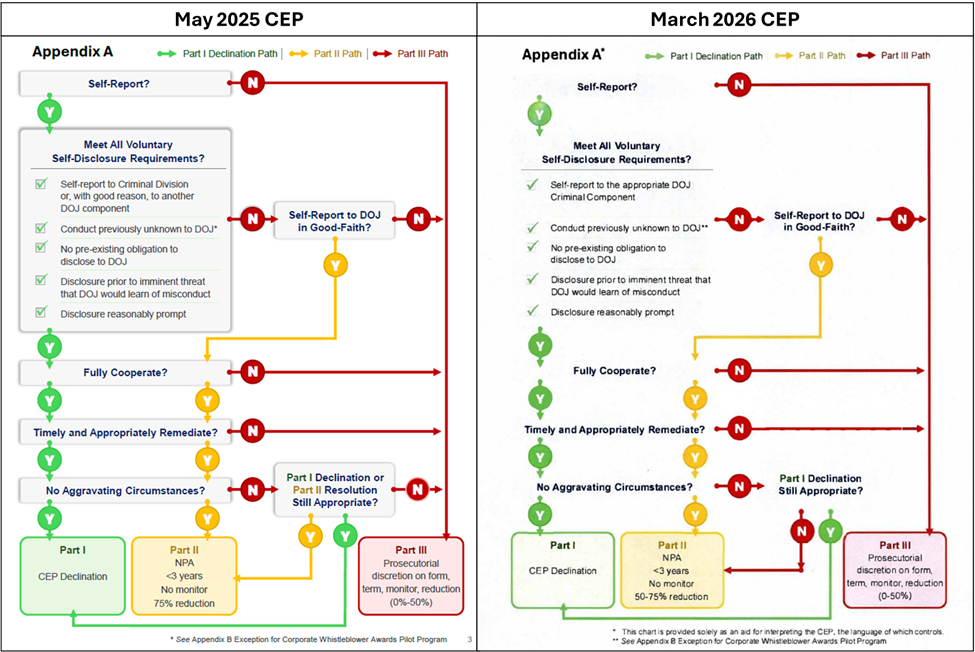

While the DOJ CEP is similar to the prior policy issued by the Criminal Division (the Criminal Division CEP), last revised in May of 2025, it introduces modifications to the resolution framework and policy shifts relating to self-disclosure requirements, cooperation standards, cooperation credit, and the Corporate Whistleblower Awards Pilot Program. The CEP reflects the DOJ’s goals of incentivizing corporate compliance while reducing resolutions that require monitors and ongoing oversight.

The DOJ CEP governs all corporate criminal matters resolved with the DOJ, except for criminal antitrust matters, and “supersed[es] all component-specific or U.S. Attorney’s Office-specific corporate enforcement policies currently in effect.” Like prior CEPs, its stated purpose is to incentivize companies to voluntarily self-disclose misconduct, cooperate with investigations, and remediate wrongdoing. All corporate resolutions must be approved by the relevant Assistant Attorney General or US Attorney in coordination with the Office of the Deputy Attorney General and the Criminal Division, as required by the Justice Manual.

Like the Criminal Division CEP before it, the DOJ CEP is divided into three parts that illustrate the different outcomes that might result from various scenarios, such as declination, non-prosecution agreements, and other resolutions. It also includes a similar flowchart illustrating the possible outcomes based on key factors.

Part I: Declination

Under Part I, DOJ will presumptively decline prosecution where a company meets four stated criteria.

The company voluntarily self-disclosed the misconduct to an appropriate DOJ criminal component.

The company fully cooperated with the Department’s investigation.

The company timely and appropriately remediated the misconduct.

There are no aggravating circumstances related to the nature and seriousness of the offense, egregiousness or pervasiveness of the misconduct within the company, severity of harm caused by the misconduct, or corporate recidivism, specifically, a criminal adjudication or resolution within the last five years based on similar misconduct by the entity engaged in the current misconduct.

The DOJ CEP did not materially alter the Criminal Division CEP’s five-part standard for what qualifies as voluntary self-disclosure.

The company must make a good faith disclosure of the misconduct to the appropriate Department component.

The misconduct is not previously known to the Department.

The company had no preexisting obligation to disclose the misconduct to the Department.

The voluntary disclosure occurs “prior to an imminent threat of disclosure or government investigation,” U.S.S.G. § 8C2.5(g)(1).

The company discloses the conduct to the Department within a reasonably prompt time after becoming aware of the misconduct, with the burden being on the company to demonstrate timeliness.

Regarding the fourth factor for presumptive declination — lack of aggravating circumstances — the DOJ CEP expanded the concept of “corporate recidivism.” It now takes into account both criminal adjudications and resolutions that were (1) based on similar misconduct and (2) from the last five years, as well as any criminal adjudication or resolution based on either similar misconduct or that occurred within the past five years.

Part II: ‘Near Miss’ Voluntary Self-Disclosures or Aggravating Factors

Part II relates to companies that fully cooperate and timely remediate but do not qualify for a Part I declination because (1) their disclosure did not meet the voluntary self-disclosure standard or (2) aggravating factors warrant a criminal resolution. In such cases, pursuant to the DOJ CEP, DOJ shall:

Provide a Non-Prosecution Agreement (NPA), absent particularly egregious or multiple aggravating circumstances.

Allow a term length of fewer than three years.

Not require an independent compliance monitor.

Provide a reduction of at least 50% but not more than 75% off the low end of the US Sentencing Guidelines (USSG) fine range.

The 50-75% fine reduction differs from the fine reduction outlined in the Criminal Division CEP, which provided for a 75% fine reduction. This change suggests that though DOJ is willing to offer fine reductions in cases of timely cooperation and remediation, it is not prepared to guarantee such a steep incentive across the board.

Notably, unlike the Criminal Division CEP, the DOJ CEP eliminates the avenue for a Part III resolution (where a prosecutor maintains discretion over the resolution form, term, monitor, and reduction) where a company has met the Part I/II requirements but there are aggravating circumstances. The Criminal Division CEP permitted a Part III resolution when there existed aggravating circumstances, regardless of whether a company had self-reported, met all voluntary self-disclosure requirements, fully cooperated, and timely and appropriately remediated. The DOJ CEP, however, provides for a Part I or Part II resolution where a company has complied with all disclosure, cooperation, and remediation requirements, despite the presence of aggravating circumstances.

Part III: Other Resolutions

Under the DOJ CEP, like the Criminal Division CEP, if a company is not eligible for a declination under Part I or an NPA under Part II, prosecutors retain full discretion over the resolution form, term length, compliance obligations, and monetary penalty. Like the Criminal Division CEP, the DOJ CEP caps the maximum available fine reduction in Part III at 50% off the USSG fine range, with a presumption that prosecutors will take the reduction from the low end for companies that fully cooperate and timely remediate.

Other Differences Between the DOJ CEP and the Criminal Division CEP

Beyond those outlined above, the DOJ CEP includes four other substantive changes from the Criminal Division CEP, all of which are important for companies to understand.

First, the DOJ CEP provides more explicit requirements and guidance for the procedures surrounding self-reporting. Specifically, it states that companies must self-disclose to the proper DOJ component to be eligible for a Part I resolution. DOJ provides for some leeway; however, if a company makes a good faith disclosure to one component where the matter is later brought to another appropriate component for investigation. Disclosures “made only to federal regulatory agencies, state and local governments, or civil enforcement agencies” will not qualify unless DOJ, in its discretion, provides an exception where there is a good faith disclosure to one of these entities.

Second, in defining “Full Cooperation,” the DOJ CEP adds that nothing in the CEP is intended to prohibit a company from taking steps that it is otherwise obligated to take under applicable laws and regulations. However, if such requirements conflict with a DOJ investigation or deconfliction request, the company is expected to notify DOJ in advance with sufficient time for it to take “reasonable steps.”

Third, the DOJ CEP includes changes to the comments regarding cooperation credit. Now, prosecutors should include in their corporate resolution agreements information sufficient to outline why a particular company received a particular amount of cooperation credit. It also states that DOJ will consider a company’s “size, sophistication, and financial condition” when assessing its level of cooperation. The DOJ CEP struck the requirement from the Criminal Division CEP that the company bear the burden to provide factual support for an assertion that its financial condition impaired its ability to cooperate more fully. As a practical matter, however, companies will likely still need to provide a factual basis for such an assertion to maximize cooperation credit.

Finally, the DOJ CEP continues to incorporate the Corporate Whistleblower Awards Pilot Program Exception, which enables a company to qualify for declination if it self-reports following a whistleblower’s internal report. However, there is one key distinction in the DOJ CEP; while the Criminal Division CEP stated that a company could benefit from the program if it self-reported the relevant conduct to DOJ within 120 days following a whistleblower’s internal report, the DOJ CEP states that a company must now report “as soon as reasonably practicable but no later than 120 days.” This will require companies to move even more quickly to conduct a full internal investigation before self-disclosing.

Practical Implications

The DOJ CEP builds upon the Criminal Division’s work and highlights the DOJ’s continued emphasis on self-disclosure and cooperation. It also comes less than two weeks after the announcement of the Southern District of New York’s CEP (SDNY CEP), which was modeled off the Criminal Division CEP but contains key differences. Specifically, SDNY’s CEP is limited in scope to fraud and financial misconduct affecting market integrity, contains categorical exclusions from declination for certain misconduct, and follows different declination procedures. While the DOJ CEP supersedes the SDNY CEP and requires coordination of all resolutions through the Criminal Division, it will be interesting to see what level of discretion, if any, the SDNY (which has, up until recently at least, operated with significant autonomy from Washington), or any of the other US Attorneys’ Offices around the country, will retain going forward. Nonetheless, DOJ’s decision to issue an overarching CEP gives companies a single guidebook for self-reporting while providing a more centralized review process and more uniform resolutions.

Full cooperation and timely and appropriate remediation remain necessary for self-disclosing companies to receive either a declination or an NPA. Companies should continue to focus on implementing effective corporate compliance programs and internal investigation procedures to swiftly and efficiently review reports. This should include ensuring the retention of accurate business records so that if misconduct is identified, companies can undertake root cause analyses and evaluate potential remediation efforts, such as disciplining employees involved in misconduct and conducting or updating training programs, on a timely basis. Experienced counsel should always be consulted when considering whether to self-disclose.

Contacts

- Related Practices